![]()

26-03-11

☁️ Oracle:杠杆的艺术

2026财年第三季度关键指标:

- ☁️营收增长加速(但存在一些问题):总营收达到 172 亿美元,同比增长 22%。按固定汇率计算,增长率仅为 18%,这意味着部分增长来自汇率波动,而非实际需求。

- 📦 积压订单持续攀升:RPO 达到 5530 亿美元,同比增长 325%,环比增长 6%。管理层还表示,许多新的 AI 合同所需的 Oracle 资金减少,因为客户选择预付款或直接提供 GPU。

- ⚡ OCI 再次加速增长:Oracle 云基础设施 (OCI) 收入同比增长 84% 至 49 亿美元,高于上一季度的 68%。云总收入增长 44% 至 89 亿美元,而多云数据库收入更是飙升 531%。

- 💵 业绩指引上调:管理层重申 2026 财年营收指引为 670 亿美元,并将 2027 财年营收指引上调 40 亿美元至 900 亿美元。

损益表:

- 营收同比增长 22% 至 172 亿美元(超出预期 3 亿美元)。

- ☁️云业务同比增长 44%,达到 89 亿美元。

- 🌐 软件行业同比增长 3%,达到 61 亿美元。

- 🖥️ 硬件同比增长 2% 至 7 亿美元。

- 💼服务业同比增长 12%,达到 14 亿美元。

- 向 IaaS 的转型将毛利率压缩至 65%(同比下降 6 个百分点)。

- 营业利润率为 32%(同比增长 1 个百分点)。

- 过去12个月的经营现金流增长了13%,达到240亿美元。

- 过去12个月的自由现金流为负250亿美元,并且由于资本支出增长,仍然面临巨大压力。

- 管理层维持 2026 财年资本支出预期不变,仍为 500 亿美元。

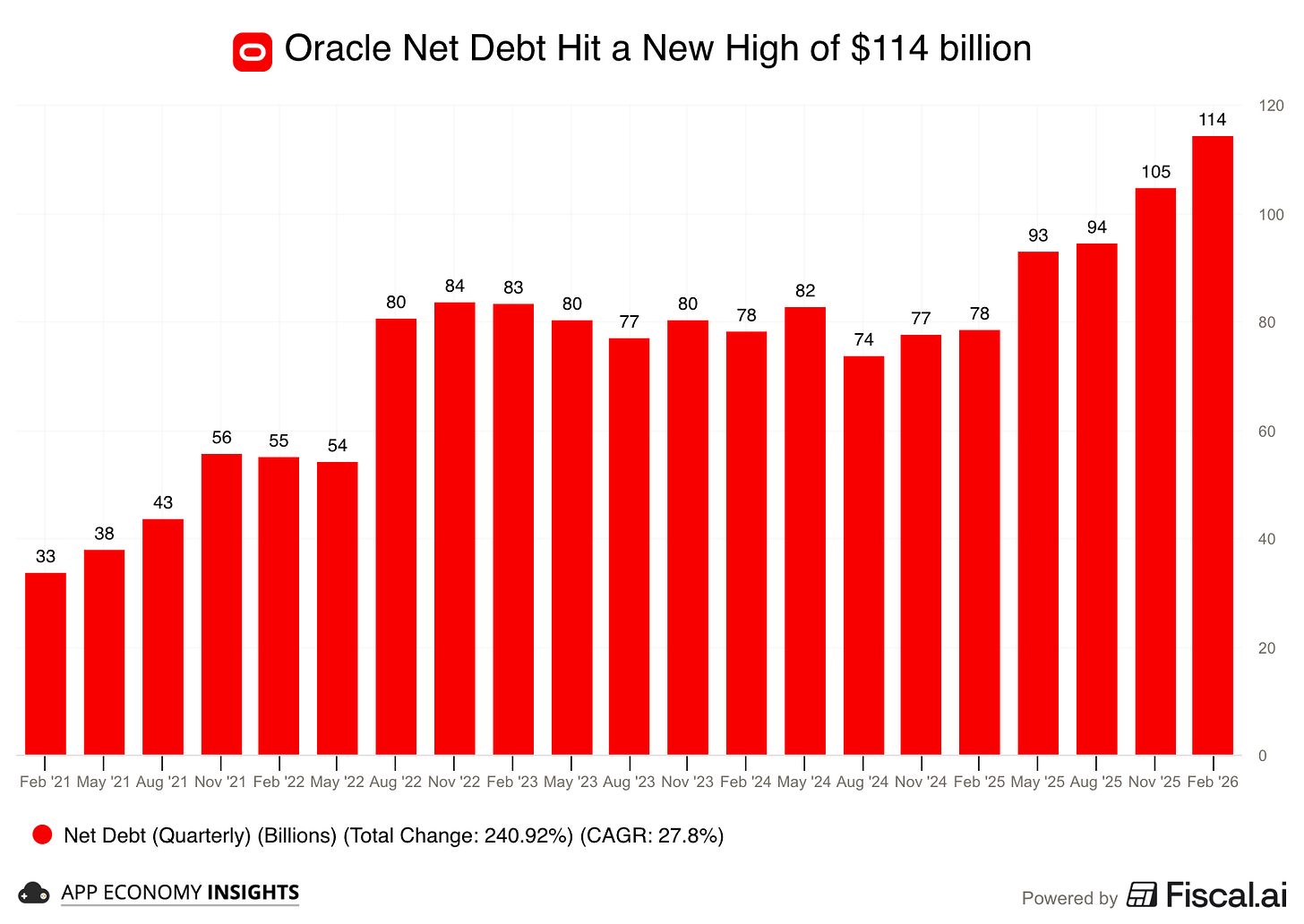

- 净债务:1140亿美元(基于280亿美元的过去12个月EBITDA,净杠杆率超过4倍)。

甲骨文公司 (NYSE: ORCL) 股票分析和业务概览

Oracle Corporation is a global technology leader specializing in enterprise software, cloud infrastructure, databases, and AI-driven solutions, serving industries such as finance, healthcare, retail, and government. Founded in 1977 and headquartered in Austin, Texas, the company operates through segments like Cloud and License (including SaaS and IaaS), Hardware, and Services, with a strong emphasis on its Oracle Cloud Infrastructure (OCI) for AI workloads, Fusion Cloud ERP/HCM applications, and Autonomous Database. Recent strategies center on aggressive AI expansion, including massive data center buildouts, partnerships with hyperscalers like Meta and Nvidia for GPU-intensive AI training, and innovations in AI-integrated applications to capture enterprise demand. Oracle's "Gen2" cloud architecture differentiates through cost efficiency, security, and multicloud interoperability, aiming to disrupt incumbents like AWS and Azure. The company employs over 140,000 people and generates revenue from over 430,000 customers in 175 countries, with cloud now accounting for half of total revenue.

Financially, Oracle delivered robust growth in Q2 FY2026 (ended November 30, 2025), with total revenue of $16.1 billion (+14% YoY in USD, +13% in constant currency), driven by cloud momentum despite a slight miss on expectations ($16.06B vs. $16.21B est.). Cloud revenue (IaaS + SaaS) surged 34% to $8.0 billion, with OCI up 68% to $4.1 billion and GPU-related revenue soaring 177% amid AI boom. Remaining Performance Obligations (RPO) exploded to $523 billion (+438% YoY), up $68 billion sequentially, reflecting massive new deals and backlog diversification. GAAP EPS rose 91% to $2.10, while non-GAAP EPS climbed 54% to $2.26, beating estimates by $0.62. Operating income grew 8% to $6.7 billion, with non-GAAP margins at ~42%. However, CapEx escalated to $12 billion in Q2, leading to negative free cash flow of -$10 billion and TTM FCF of -$13 billion, as Oracle invests heavily in AI infrastructure. FY2026 guidance anticipates total revenue >$67 billion (+16%), cloud growth >40%, OCI >70%, and CapEx >$25-50 billion to meet demand. Strengths include high-margin recurring revenue (~92% from subscriptions), AI leadership in enterprise databases, and a $500+ billion RPO backlog for visibility. Risks encompass mounting debt nearing $100 billion, a potential $6.6 billion liquidity gap, economic sensitivity, and competition in cloud/AI, plus legal headwinds like lawsuits. Overall, Oracle's pivot to AI-cloud dominance positions it for 15-20% annual growth in a $1 trillion+ enterprise software market, though execution on CapEx and debt management is critical.

Stock Price Analysis and Analyst Outlook

As of January 16, 2026, ORCL shares closed at $191.09, up 0.65% (+$1.24) from the previous close, with after-hours trading at $190.85 (-0.13%). The stock is near the lower end of its 52-week range ($118.86-$345.72), down ~40% from all-time highs amid debt concerns and post-Q2 volatility. Recent performance shows a YTD 2026 decline of ~3.23%, a 1-month gain of ~4.24%, but a 6-month drop of ~23.10%, reflecting mixed sentiment on AI growth versus financial strains. Trading volume on January 16 was ~19.2 million shares, above average, with the stock crossing below its 50-day (~$203) and 200-day (~$241) moving averages, signaling bearish trends.

Key valuation metrics indicate potential undervaluation for a growth-oriented tech giant:

- Market Cap: ~$549 billion

- Trailing P/E: 35.99

- Forward P/E: ~22-25 (based on FY2026 EPS est.)

- Trailing EPS: $5.31; Forward EPS: $5.00-$5.61 (FY2026), implying 12-32% growth

- Dividend Yield: 1.05% ($2.00 annualized)

- Beta: 1.65

Analyst sentiment remains predominantly bullish, viewing the dip as a buying opportunity amid AI tailwinds, with a consensus "Moderate Buy" or "Buy" from 43 analysts. Ratings break down to ~31 Buy, 10 Hold, and 2 Sell. Average price targets range from $292-$305, implying 53-60% upside from current levels, with highs at $400 (e.g., Jefferies, Mizuho; ~109% potential) and lows around $175-195. Recent adjustments include KeyCorp lowering to $300 (Overweight), Royal Bank to $195 (Sector Perform), and Bank of America to $300 (Buy), citing debt risks but optimism on cloud execution. Technically, oversold signals (e.g., Stochastic Oscillator) suggest possible rebound, with support near $186 and resistance at $200. Catalysts include Q3 FY2026 earnings (expected March 9, 2026) and debt management updates. Overall, ORCL merits a Buy for long-term investors betting on AI-driven recovery, with potential to hit $250-$300 in 2026 if cloud growth accelerates, though near-term debt and volatility pose risks.

24-11-19:

业务概览

Oracle Corporation 是一家领先的企业技术提供商,专门提供数据库管理、云服务和企业软件解决方案。该公司在云计算方面取得了重大进展,其 Oracle 云基础设施 (OCI) 和 Oracle Fusion 应用程序已成为核心增长动力。此外,该公司还在其产品中嵌入了 AI 功能,增强了其对寻求可扩展智能系统的企业的吸引力。

近期业绩及财务指标

- 收入增长:甲骨文报告称,2024 年其年收入为 592.3 亿美元,同比增长 11.8%,预计由于对云和人工智能驱动产品的强劲需求,2025 年将达到 663.5 亿美元。

- 收益:2024 年每股收益 (EPS) 为 6.41 美元,较 2023 年大幅增长 72.8%。预计 2025 年每股收益将增长 13.8% 至 7.30 美元。

- 云计算增长:Oracle 的云计算部门继续保持强劲增长,得益于与微软等主要组织在数据库集成和政府合同方面的合作。

市场与估值

- 当前股价:约 185.73 美元(截至 2024 年 11 月),使 Oracle 成为价格较高的蓝筹科技股之一。

- 估值:分析师预计平均目标价为 175.13 美元,这意味着可能下跌约 5.7%。不过,看涨情景预测高点为 205 美元,这意味着上涨空间约为 10%。

- 一致评级:尽管对竞争和估值存在一些担忧,但甲骨文仍获得分析师的“买入”评级,这得益于其强劲的云计算增长和人工智能集成。

战略举措

Oracle 积极瞄准人工智能和云计算市场,利用生成式人工智能和可扩展的云解决方案来推动采用。它还继续扩展其 Fusion Cloud 供应链和制造功能以及数据库服务,以满足商业和政府部门的需求。

投资考量

- 看涨因素:

- 云计算和人工智能服务强劲增长。

- 强劲的财务业绩和每股收益增长。

- 战略合作伙伴关系和大规模人工智能应用。

- 看跌风险:

- 来自微软、亚马逊和谷歌在云计算领域的竞争压力。

- 与同行相比估值较高。

结论

由于在云计算和人工智能技术方面的投资,甲骨文在长期增长方面处于有利地位。投资者应权衡其溢价估值与其持续增长潜力,并考虑其作为稳定、创新驱动型企业参与者的角色。分析师大多看好该股,尤其是那些具有长期眼光并对云计算和人工智能市场感兴趣的分析师。

No comments:

Post a Comment